Australia prides itself on being the land of the fair go. Yet inequality has risen steadily for nearly half a century, with over 3.5 million Australians living in poverty, while the wealth of Australia’s 200 richest people has tripled in the last 20 years.

For too long, our tax system has exacerbated rather than alleviated inequality by taxing wealth too lightly and labour too heavily. Three prime offenders are the tax concessions that the government has targeted in this year’s budget reforms. The capital gains tax discount, negative gearing, and discretionary trusts have long enabled well-heeled and well-advised taxpayers to effectively choose how much tax they pay on gains made from equity and housing. People who work for a living are not awarded such luxury in providing the revenue needed to fund essential services.

Much discussion around the budget has focused on intergenerational equity, but the issue is also one of intra-generational equity: not all boomers are riding the crest of a tax-subsidised asset boom, with older single women the fastest growing category of homeless.

Meanwhile, some lucky millennials will have access to tax-free gifts and inheritances in the ‘great wealth transfer’ of between $3.5-$5.4 trillion to be handed down between generations over the next 20 years.

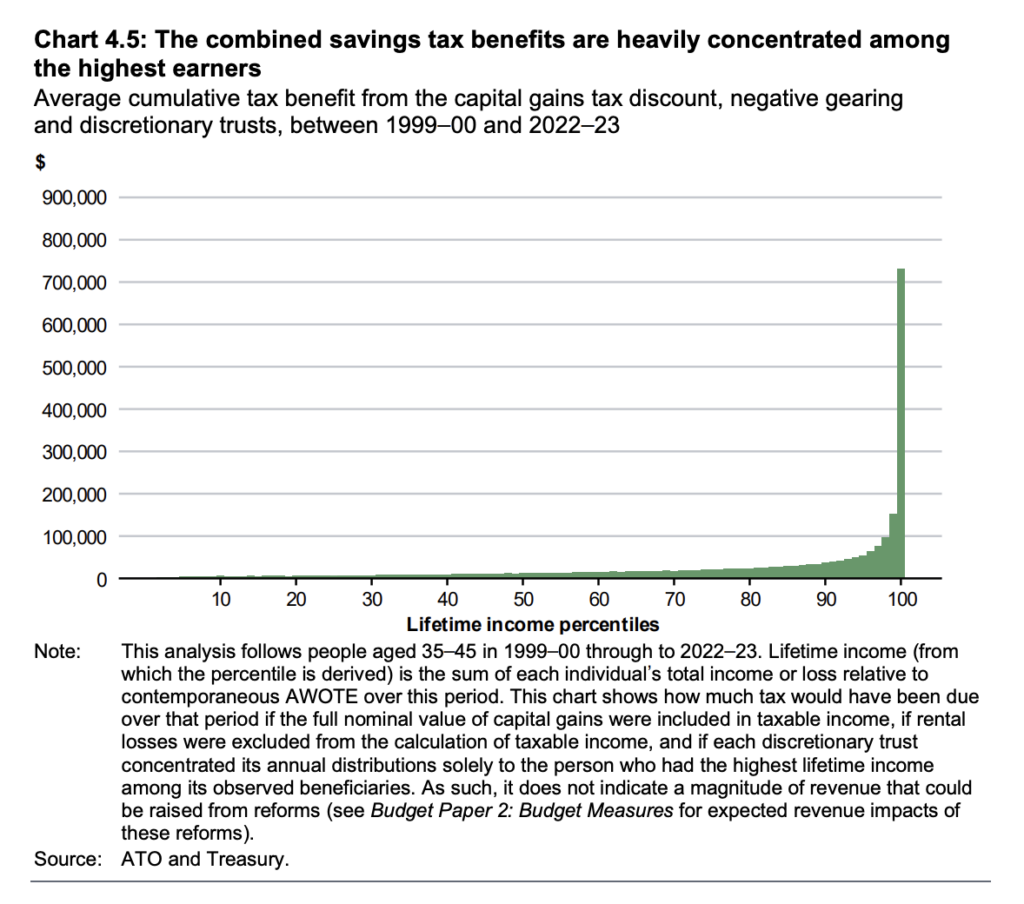

Not only are these concessions expensive, foregoing more than $50 billion in revenue for 2025-2026, they are unfair – with the benefits overwhelmingly going to the top 10 percent of income earners, with the gains concentrated at the top 1 per cent.

Imagine a government proposal to spend more than $50 billion a year subsidising the investment activities of the wealthiest 10 per cent of Australians. It would be politically unthinkable. Yet that is effectively what we do when we provide the same support through tax concessions rather than direct spending.

Rather than just taxing all gains the same, be that a buck from the sale of a share or from the sale of your labour, these concessions reward tax planning over genuine productivity. They give those who earn income from capital the choice to minimise their taxable income, leaving the bill to those who only earn income from labour.

By way of example, let’s compare three scenarios.

A nurse who earns $100k from work will pay an effective tax rate of 20.8%.

How about someone whose sole income is from real estate investments? Let’s say they earned $100k from flipping a property. They’ll pay just $5,788 on that capital gain, so an effective tax rate of 5.8%.

What about trusts? An individual who buys and sells a share portfolio through a discretionary trust for a $100k gain can distribute the gain equally between a domestic partner and two adult children and pay no tax. Zero.

Discretionary trusts have long been the beating heart of tax planning for the very rich. 90 percent of the value in private trusts goes to those in the top 10 percent of Australian households. Compare this with the fact that over 95 percent of Australians do not receive income from a discretionary trust.

The reforms will close loopholes that reward tax planning over genuine productivity. The capital gains tax discount of 50% would be replaced with indexation to inflation, subject to a minimum of 30% tax. Negative gearing would be limited to offset only investment rather than labour income. Discretionary trusts would be taxed at a minimum of 30%, narrowing the ways they can be used to minimise tax.

These reforms should apply to all assets, shares and property alike, without carve outs and special treatment. For the past half-century economists have come up with numerous arguments for why the rich should pay less tax – they’ll work less, they’ll invest less, they’ll relocate. In practice, none of these claims have been proven. At best, what we can say is that when we try to tax the rich, they try to avoid it. In response, we need fewer, not more loopholes. Why shouldn’t all forms of income be taxed like our wages are?

Tax reform in the collective interest will rarely produce champions in support and regularly produce opponents who stand to lose from change. Let’s be clear that, despite the noise, these reforms target concessions that overwhelmingly benefit the top 10 and 1 percent. If Australia wants to avoid the social and political fracturing we see elsewhere, we collectively need to get behind these tax reforms before inequality gets the better of us.

Kathryn James is an Associate Professor at the Melbourne Law School, University of Melbourne.